10000 20000 3000 5000 38000. Thus the overhead allocation formula is.

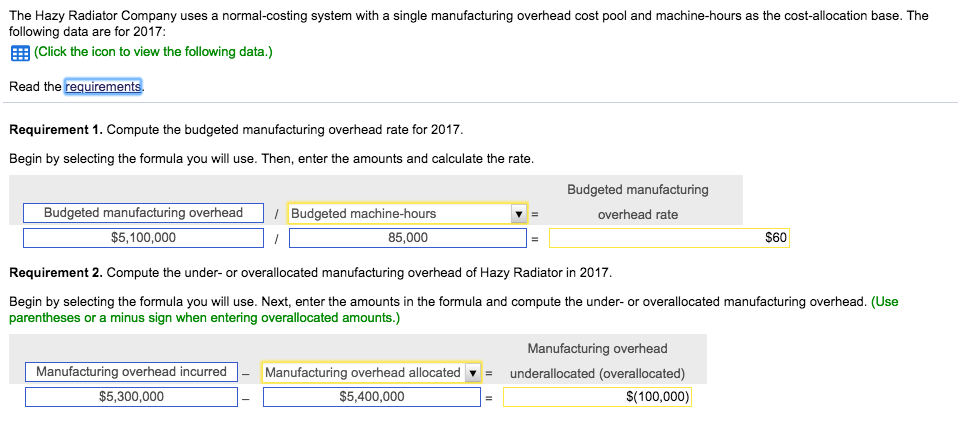

Solved Data Table Budgeted Manufacturing Overhead Costs O Chegg Com

Calculate the manufacturing overhead.

How to calculate manufacturing overhead allocated. Before you can calculate manufacturing overhead for WIP you need to determine the WIP ending balance. Usually budgeted figures are used to calculate the overhead absorption rate. Lets illustrate an overhead rate based on direct labor hours for a company that manufactures just two products X and Y.

While some of these costs are fixed such as the rent of the factory. Firstly determine the cost of goods sold which includes all direct and indirect costs of production. Next determine the cost of raw material which includes the cost of raw material purchase.

Add up total overhead. Next determine the cost of raw material. Manufacturing overhead includes indirect manufacturing costs such as repairs and scrap depreciation.

14500 200000 x 100 725 The calculation result means that 725 of sales revenue will need to go toward. Fixed costs on the other hand are all costs that are not inventoriable costs. Calculate the direct cost of goods sold.

First determine the COGS. The estimated amount of overhead costs are the costs that cannot be allocated specifically to any of the product department or object are to be applied to different jobs. The formula is the WIP beginning balance plus manufacturing costs minus the cost of goods completed.

The typical procedure for allocating overhead is to accumulate all manufacturing overhead costs into one or more cost pools and to then use an activity measure to apportion the overhead costs in the cost pools to inventory. Compute the overhead allocation rate by dividing total overhead by the number. All we need to do is add all the costs.

It generally includes rent of the production unit wages and salaries paid to factory employees and managers quality department employees expenses people who inspect the products electricity. The base units estimated activity is the basis on which the companys overhead is to be applied. The total manufacturing overhead of 50000 divided by 10000 units produced is 5.

To find the manufacturing overhead per unit In order to know the manufacturing overhead cost to make one unit divide the total manufacturing overhead by the number of units produced. For example if the total overhead for making a product is 500 and the total direct labor hours is 150 hours the overhead allocation rate is. Calculate the cost of raw material.

These are mostly fixed in nature and incur along with the start of the production unit. To allocate the overhead costs you first need to calculate the overhead allocation rate. Manufacturing Overhead are the costs incurred irrespective of the goods manufactured or not.

Select an allocation base. Therefore the method does not involve additional clerical work. Therefore the manufacturing overhead is 38000.

Factory overhead is the costs incurred during the manufacturing process not including the costs of direct labor and direct materials. To help you keep uneven allocations straight remember that overhead allocation entails three steps. 175000 10000 1750 This means that Joes overhead rate using machine hours is 1750 so for every hour.

By allocating manufacturing overhead on the basis of direct labor hours a product requiring 30 direct labor hours would be allocated twice as much manufacturing overhead as a product requiring 15 direct labor hours. Calculate the total manufacturing overhead costs. To allocate these costs to your inventory items divide the manufacturing overhead by an.

Factory overhead is normally aggregated into cost pools and allocated to units produced during the period. How Do You Calculate Allocated Manufacturing Overhead. This is done by dividing total overhead by the number of direct labor hours.

The following are the advantages in using predetermined overhead absorption rate. The allocation base is the basis on which a business assigns overhead costs to products. The formula for manufacturing overhead can be derived by using the following steps.

Firms use predetermined overhead absorption rate computed for a normal period usually one year of business activity. Calculate manufacturing overhead to be allocated based on direct labor cost to from ACG 2071 at University of Florida. To calculate the overhead rate using machine hours do the following calculation.

Suppose you start the year with 25000 worth of WIP and incur 300000 in manufacturing costs. This step requires adding indirect materials indirect labor and all other product costs not. The cost of completed goods comes to 305000.

Generally this is the labor hours or machine hours but it could be another method that the business thinks best. Here is the formula for calculating your monthly manufacturing overhead rate. Cost pool Total activity measure Overhead allocation per unit.

Activity Based Vs Traditional Costing

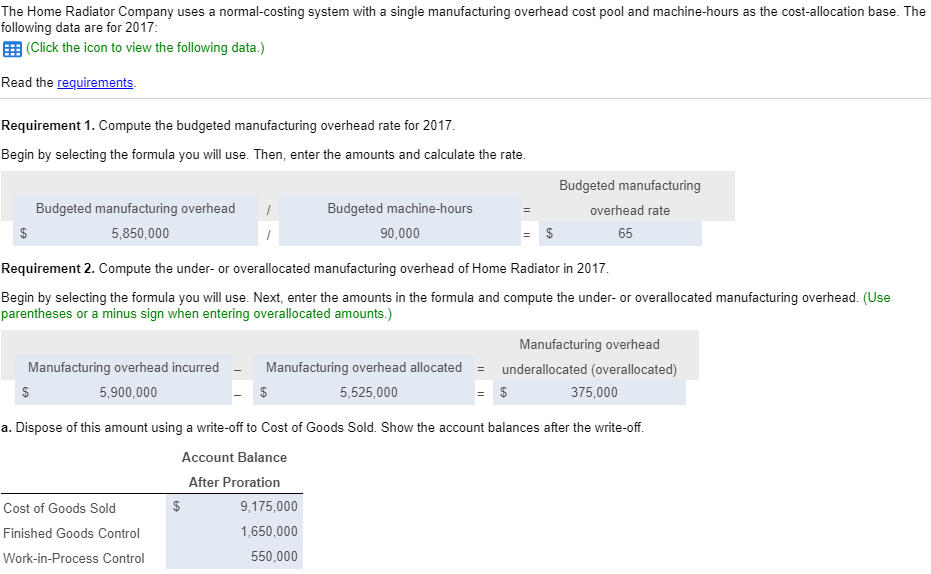

Solved Budgeted Manufacturing Overhead Costs 5 850 000 Ov Chegg Com

Applied Overhead Predetermined Rate Double Entry Bookkeeping

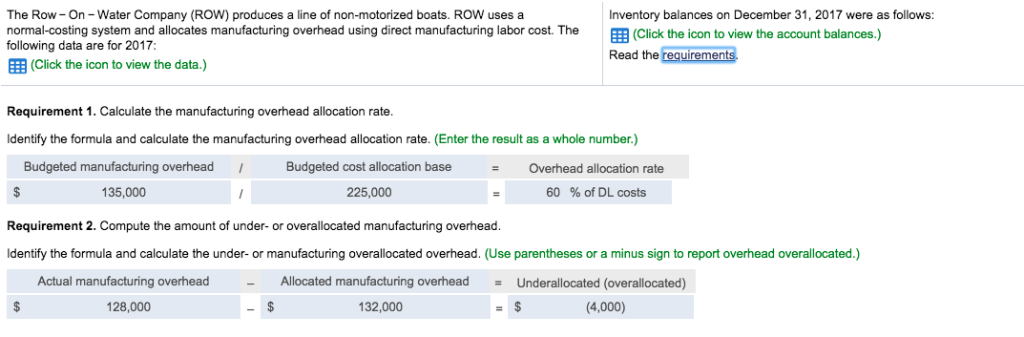

Solved The Row On Water Company Row Produces A Line Of Chegg Com

Chapter 17 Accounting Ii