Contribution margin per unit formula would be Selling price per unit Variable cost per unit 6 2 4 per unit. Some people think that the contribution margin is only useful for firms with high fixed costs.

Contribution Margin Wikipedia

Contribution Margin Ratio Formula.

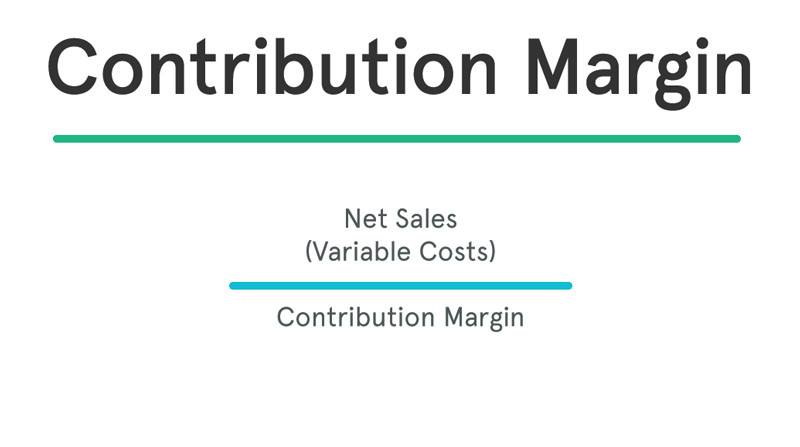

Variable cost contribution margin. Contribution Margin Net Sales Revenue Variable Costs. Contribution margin CM is the amount by which a products sales exceeds its variable costs. Heres an example of how to solve for contribution margin.

This concept is one of the key building blocks of break-even analysis. The contribution margin sometimes used as a ratio is the difference between a companys total sales revenue and variable costs. To generate this as a.

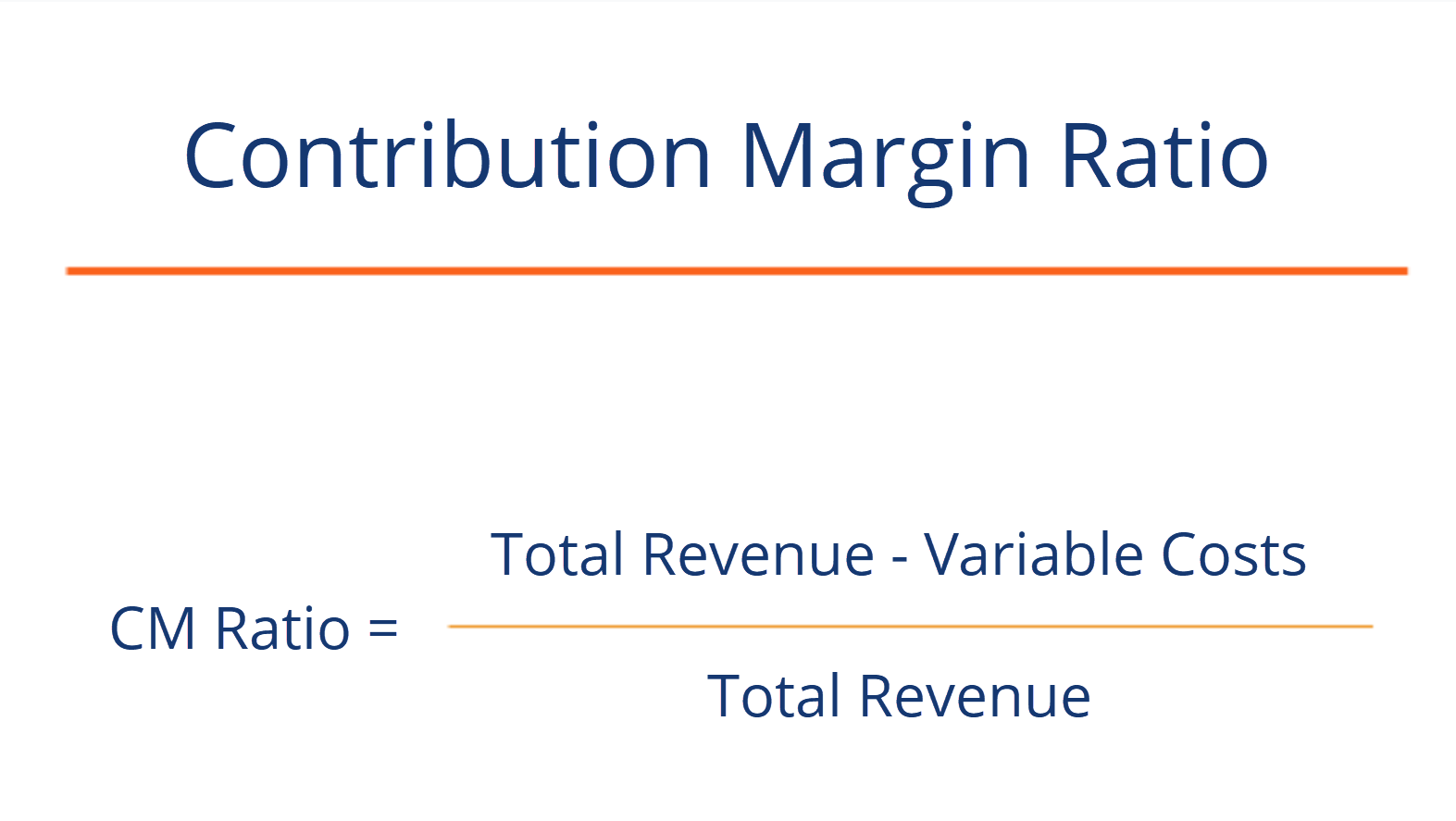

The contribution margin is the amount of money a business has to cover its fixed costs and contribute to net profit or loss after paying variable costs. Contribution Margin Ratio Net Sales Revenue -Variable Costs Sales Revenue Sample Calculation of Contribution Margin. Dalam contoh yang disajikan contribution margin dari setiap pasang sepatu rajut yang terjual dapat dihitung seperti berikut.

Variable contribution margin is the margin that results when variable production costs are subtracted from revenue. To calculate the variable contribution margin perform the following calculation. If a product sells for 100 and its variable cost is 35 then the products contribution margin is 65.

Revenue Management may also want to calculate the contribution margin on a per-unit basis. It is expressed either as total contribution margin contribution margin per unit or contribution margin ratio. It represents the incremental money generated for each productunit sold after deducting the variable portion of the firms.

This is the sales amount that can be used to or contributed to pay off fixed costs. Total variable expenses include both manufacturing and non-manufacturing variable expenses. Contribution ratio would be Contribution Sales 200000 300000 23 6667.

It is used to find an optimal price point for a product. Contribution margin CM s the selling price per unit minus the variable cost per unit. This left-over value then contributes to paying the periodic fixed costs of the business with any remaining balance contributing profit to the owners.

In accounting the terms sales and less all variable costs Fixed and Variable Costs Cost is something that can be classified in several ways depending on its nature. Contribution margin revenue variable costs For example if the price of your product is 20 and the unit variable cost is 4 then the unit contribution margin is. It is most useful for making incremental pricing decisions where an entity must cover its variable costs though not necessarily all.

Contribution represents the portion of sales revenue that is not consumed by variable costs and so contributes to the coverage of fixed costs. The variable cost per unit is 2 per unit. Contribution would be 4 50000 200000.

The contribution margin can be stated on a gross or per-unit basis. To determine the ratio. Contribution represents the portion of sales revenue that is not consumed by variable costs and so contributes to the coverage of fixed costs.

Therefore you have a variable contribution margin of 20. The formula for contribution margin is the sales price of a product minus its variable costs. Contribution margin is the amount left-over after deducting from the revenue the direct and indirect variable costs incurred in earning that revenue.

In a service firm contribution margin is equal to revenue from provision of services less all variable expenses incurred to provide such services. The contribution margin is the sales price of a unit minus the variable costs involved in the units production. Variable costs are costs which vary directly with sales.

For this you would use the same formula but input the values for one unit. The contribution margin ratio CM ratio of a business is equal to its revenue Sales Revenue Sales revenue is the income received by a company from its sales of goods or the provision of services. Contribution margin is equal to sales revenue less total variable expenses incurred to earn that revenue.

Contribution Margin Fixed Costs Net Income. Its a simple calculation. This represents the margin available to pay for fixed costs.

In other words calculating the contribution margin determines the sales amount left over after adjusting for the variable costs of selling additional products. In other words the contribution margin equals the amount that sales exceed variable costs. 30 - 4 1 5 20.

It is the net amount available to cover the fixed costs and target profit. Contribution margin CM or dollar contribution per unit is the selling price per unit minus the variable cost per unit. Ratio dfrac Sales.

You can also express the contribution margin as a percentage by using the following formula. Contribution margin Harga produk Biaya variabel per unit Rp 150000- Rp 62000- Rp 88000-Dari perhitungan di atas diperoleh nilai contribution margin sebesar Rp 88000- per unit produk. Sales price - variable costs variable contribution margin.

Contribution Margin Definition Formula Analysis Contribution Margin Ratio Gross Margin

Contribution Margin Ratio Formula Per Unit Example Calculation

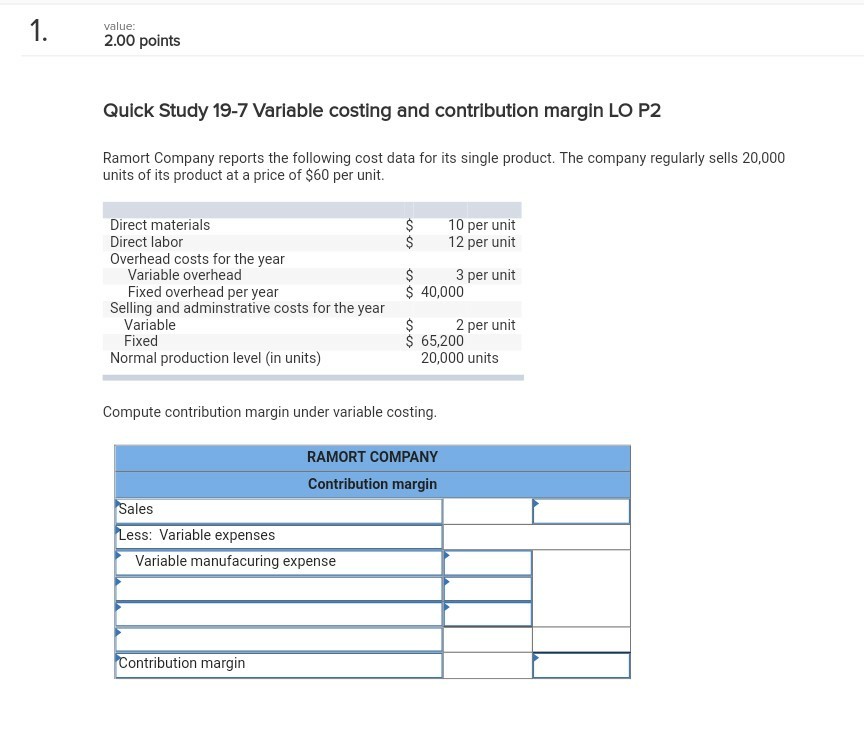

Solved Value 2 00 Points Quick Study 19 7 Variable Costin Chegg Com

How To Compute Contribution Margin Dummies

Contribution Margin Ratio Revenue After Variable Costs